The recent hurricane Ian impacted much of the southeast United States. As a result, it is good to know the general tax rules related to disaster victims. Below, we look at several tax topics for disaster area victims.

The recent hurricane Ian impacted much of the southeast United States. As a result, it is good to know the general tax rules related to disaster victims. Below, we look at several tax topics for disaster area victims.

1. Tax Returns and Filings

Q: I am a disaster area victim and needed to move from my home. I might not be back for a long time or even at all. Which address should I use on my tax return?

A: A taxpayer should always use their current address in filing a tax return. In the situation where you move after filing your return, you need to update your address with the IRS. You can do this either by filing form 8822 or calling the IRS Disaster Hotline at 866-562-5227.

Q: I filed an extension for my form 1040, giving me until Oct. 15 to file. Are there any further extensions available?

A: Taxpayers who already filed for an extension until Oct. 15 and live in a federally declared disaster area of the recent hurricanes receive an automatic extension due date of Dec. 31.

2. Payments

Q: I have a balance due on my 2021 tax return and am currently accruing interest on it. Is there any relief for disaster victims on interest charges?

A: No, the IRS is not giving any forbearance or cancellation of interest on tax balance liabilities. The IRS is, however, willing to waive late payment penalties when the taxpayer can prove the reason they are late is caused by issues related to the disaster.

3. Property and Casualty Loss

Q: During a recent disaster we lost electricity and all the food in my refrigerator and freezers spoiled and I had to throw it away. My homeowners’ insurance reimbursed me, and it was for more than the food cost me. Do I have to report any income on the amount over my food costs?

A: No. The tax code makes a distinction between scheduled property and general reimbursements. For unscheduled property (general reimbursements), the taxpayer does not need to recognize income for reimbursements on personal property, even if it was more than the cost of the lost property.

Q: I need to prove the reasonable value (FMV) of my home. Am I allowed to use property tax assessments to substantiate the FMV of my home?

A: No, the only way a taxpayer can establish the FMV of a property is either with an appraisal by a credentialed appraiser or using the cost of repairs method.

4. Sale of Home

Q: My primary residence was destroyed and the cause was deemed to be a federally declared disaster. After clearing the lot, I sold the land alone for a gain. Do I have to pay taxes on the gain or is there an exclusion since it is where my primary residence used to be?

A: Selling a vacant lot does not qualify for the exemption on gains from primary residences. The exception to this rule is if the land previously had the taxpayer’s main residence on it. In this case, if the taxpayer would have qualified for the main residence exemption before the disaster, the gain on the sale of the vacant land would be exempt here as well.

5. Expenses

Q: I worked in a federally declared disaster area and had to move for my job at my own expense. Can I deduct my travel and related expenses?

A: The answer depends on whether or not the move is expected to last for more than one year. If you expect the move to be temporary, defined as less than one year, then there is no change in your tax home. In this case, you can deduct travel and related expenses to get you both to and back from your temporary work assignment. If the move is long-term, defined as more than one year, then the expenses are not deductible, regardless of whether your employer reimbursed you.

It is all about how much you keep after taxes – not what you earn from your job, a business or investments. While it is always great to see fabulous investment gains, the only financial metric that really matters is what is in your bank account at the end of the day. One of the ways you can influence this is by minimizing the taxes you pay on your investments.

It is all about how much you keep after taxes – not what you earn from your job, a business or investments. While it is always great to see fabulous investment gains, the only financial metric that really matters is what is in your bank account at the end of the day. One of the ways you can influence this is by minimizing the taxes you pay on your investments.

One highlight of the recently passed Inflation Reduction Act of 2022 (IRA; HR 5376) includes modifications to what is more commonly referred to as EV credits. Specifically, Section 30D of the Act is where the most important modifications are, and where the present tax credit for electric vehicles is spelled out in the U.S. Code. There is also new stimulus for previously owned electric vehicles, industrial vehicles and “alternative fuel refueling property.”

One highlight of the recently passed Inflation Reduction Act of 2022 (IRA; HR 5376) includes modifications to what is more commonly referred to as EV credits. Specifically, Section 30D of the Act is where the most important modifications are, and where the present tax credit for electric vehicles is spelled out in the U.S. Code. There is also new stimulus for previously owned electric vehicles, industrial vehicles and “alternative fuel refueling property.”

Despite borrowing massive amounts of money, the government still needs to find ways to raise revenue to pay for new programs and spending. The current democratically controlled Congress is looking to potentially implement new social programs and a climate bill. As a way of funding these initiatives, they are considering an expansion of the Net Investment Income Tax (NIIT).

Despite borrowing massive amounts of money, the government still needs to find ways to raise revenue to pay for new programs and spending. The current democratically controlled Congress is looking to potentially implement new social programs and a climate bill. As a way of funding these initiatives, they are considering an expansion of the Net Investment Income Tax (NIIT).

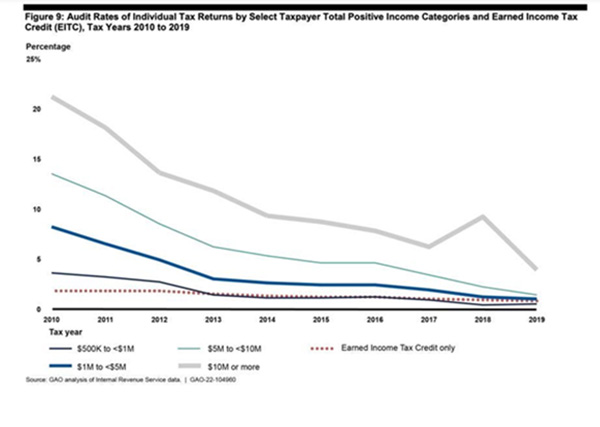

One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

COVID-19 impacted the economy dramatically and commercial real estate was no exception in terms of decreased values. Often, the real property could no longer service the debt used to finance it. This debt restructuring and resulting debt forgiveness can result in taxable income.

COVID-19 impacted the economy dramatically and commercial real estate was no exception in terms of decreased values. Often, the real property could no longer service the debt used to finance it. This debt restructuring and resulting debt forgiveness can result in taxable income.

At the very end of March, the House of Representatives passed a version of the bill known as Secure 2.0. The bill passed the House with overwhelming bipartisan support in a 414-5 vote. The House version still needs to pass in the Senate, where there are differing ideas on exactly what the bill should contain. There is strong support, so it is less of a question of if Secure 2.0 will become law than what exact version.

At the very end of March, the House of Representatives passed a version of the bill known as Secure 2.0. The bill passed the House with overwhelming bipartisan support in a 414-5 vote. The House version still needs to pass in the Senate, where there are differing ideas on exactly what the bill should contain. There is strong support, so it is less of a question of if Secure 2.0 will become law than what exact version.

The IRS is currently suffering a severe backlog in processing returns from 2021 for the 2020 tax year. As of Dec. 31, there were still more than 6 million unprocessed individual returns with notices and pending refunds. There are a few things every taxpayer should know that can help them navigate any delays in filing or speeding up the process to make filing this year as smooth as possible.

The IRS is currently suffering a severe backlog in processing returns from 2021 for the 2020 tax year. As of Dec. 31, there were still more than 6 million unprocessed individual returns with notices and pending refunds. There are a few things every taxpayer should know that can help them navigate any delays in filing or speeding up the process to make filing this year as smooth as possible.

The taxation of legal settlements and fees is a complex topic. While the mechanics to make a proper claim are now easier, the rules are still complex. Below we look at six rules to consider when it comes to the taxation of legal settlements and the deduction of legal fees on your taxes.

The taxation of legal settlements and fees is a complex topic. While the mechanics to make a proper claim are now easier, the rules are still complex. Below we look at six rules to consider when it comes to the taxation of legal settlements and the deduction of legal fees on your taxes.

No one knows for sure what 2022 will bring in the form of tax legislation, but there is certain to be some action. Top tax analysts think there are several topics that are likely to come up in 2022. Most predict that a lot of potential changes that were discussed but never made much traction in 2021 will be revisited.

No one knows for sure what 2022 will bring in the form of tax legislation, but there is certain to be some action. Top tax analysts think there are several topics that are likely to come up in 2022. Most predict that a lot of potential changes that were discussed but never made much traction in 2021 will be revisited.