One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

One of the perennial fears of taxpayers is getting audited by the IRS. Financially, few scenarios strike such fear into the heart of taxpayers. However, taxpayers can probably breathe a sigh of relief – at least for now. This is because the rate at which the IRS is initiating audits of individual taxpayers is dropping like a stone.

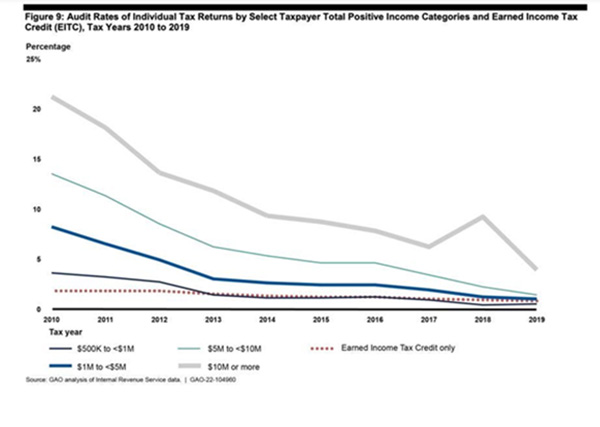

Decline in Audit Rates

The rate at which the IRS is auditing individual taxpayers has declined overall between the years of 2010 and 2019 (2020 data is too new and 2021 returns are still being filed through the extension period). According to the Government Accountability Office (GAO), nearly 1 percent of all taxpayers were audited in 2010 compared to only 0.25 percent for the tax year 2019. The GAO chart below shows the ski slope-like drop in individual tax audit rates over the period.

While the IRS continues to audit higher earning taxpayers more often overall, during the 10-year period audit rates consistently declined for all levels of taxpayers, except those with the highest incomes. The audit rate for taxpayers with income between $200k and $500k experienced the largest drop, with the audit rate declining from 2.3 percent down to 0.2 percent; a 92 percent reduction in audits. Taxpayers with the highest incomes, defined as $10 million or more, saw a resurgence in audit rates from 2017-2018; however, even they experienced an overall decline, dropping from 21.2 percent in 2019 to only 3.9 percent in 2019 – equating to an 81 percent decline.

Impact on the Treasury

There is the theory that the prospect of a tax audit leads to greater voluntary compliance. In other words, if people think they won’t get audited, then they are more likely to cheat on their taxes.

Non-compliance with tax laws and regulations have a material impact on the Treasury. According to the IRS, it is estimated that on average, individual taxpayers under-reported nearly $250 billion a year for the period 2011-2013. This obviously leads to the non-collection of taxes that are otherwise owed the government and raises issues of fairness for taxpayers who are playing by the rules.

Why the Decline in Audit Rates?

One of the main drivers is a lack of resources at the IRS, a combination of both reduced funding and less auditors on staff. The number of agents working for the IRS has declined across the board since 2011. Tax examiners, the type who handle basic audits by mail, have dropped by 18 percent. Meanwhile, revenue agents, who handle the more complex cases in the field, declined by more than 40 percent over the same period.

Demographics point to an increase in these trends as there are a wave of coming retirements in the IRS. Over the next three years, nearly 14 percent of current tax examiners and 16 percent of revenue agents are expected to retire. Stack on top of this the fact that the inexperience of newer agents and the time to complete audits is also taking longer.

Conclusion

The IRS claims it is missing out on millions in legally due tax revenues due to the inability to maintain enforcement. They say they need more funding to hire more agents to perform more audits, which not only find fraud in the audits themselves but also increase overall compliance due to the pressure this creates.

Currently, there is no political focus on bringing major new resources to the IRS, so it’s not likely to see an uptick in individual tax audit rates anytime soon. The trend of focusing on the highest earners, however, will likely continue as this is where the IRS can find the most bang for its buck.

Corporate profits, according to the Bureau of Economic Analysis, grew by $20.4 billion in the final quarter of 2021, a 0.7 percent increase. For the first quarter of 2022, corporate profits fell by 2.3 percent or $66.4 billion. On an annualized basis, corporate profits fell 5.2 percent in 2022, but grew 25 percent in 2021. With the economy facing inflation, the uncertainty of the Russia/Ukraine conflict, and the world working its way out of the COVID-19 pandemic, economic uncertainty abounds. For companies, measuring margins is one way to evaluate performance and strategize ways to survive and thrive in a dynamic economy. Here are a few common margins that businesses can determine to measure their financial performance.

Corporate profits, according to the Bureau of Economic Analysis, grew by $20.4 billion in the final quarter of 2021, a 0.7 percent increase. For the first quarter of 2022, corporate profits fell by 2.3 percent or $66.4 billion. On an annualized basis, corporate profits fell 5.2 percent in 2022, but grew 25 percent in 2021. With the economy facing inflation, the uncertainty of the Russia/Ukraine conflict, and the world working its way out of the COVID-19 pandemic, economic uncertainty abounds. For companies, measuring margins is one way to evaluate performance and strategize ways to survive and thrive in a dynamic economy. Here are a few common margins that businesses can determine to measure their financial performance. Starting June 1, the Fed began reducing its balance sheet holdings of U.S. Treasuries by $30 billion a month for three months. Thereafter, it will double its reduction of U.S. Treasuries by $60 billion per month beginning in the fourth month. For its mortgage-backed securities, the first three months will see $17.5 billion roll off its balance sheet. Starting in the fourth month of the program, this cap will increase to $35 billion per month. As its dual mandate is to both maintain employment and a stable rate of inflation, this is another way the Fed is implementing its monetary policy to put the brakes on inflation and reign in out-of-control demand with limited supply. How will the Fed’s unwinding of its balance sheet impact markets for the rest of 2022?

Starting June 1, the Fed began reducing its balance sheet holdings of U.S. Treasuries by $30 billion a month for three months. Thereafter, it will double its reduction of U.S. Treasuries by $60 billion per month beginning in the fourth month. For its mortgage-backed securities, the first three months will see $17.5 billion roll off its balance sheet. Starting in the fourth month of the program, this cap will increase to $35 billion per month. As its dual mandate is to both maintain employment and a stable rate of inflation, this is another way the Fed is implementing its monetary policy to put the brakes on inflation and reign in out-of-control demand with limited supply. How will the Fed’s unwinding of its balance sheet impact markets for the rest of 2022? Often the first house a person buys is an affordable condominium, townhouse or older single-family dwelling, also referred to as a “starter home.” It might be small and lack features they dream about, from new appliances in the kitchen, to dual sinks in the bath, to a large yard or a garage.

Often the first house a person buys is an affordable condominium, townhouse or older single-family dwelling, also referred to as a “starter home.” It might be small and lack features they dream about, from new appliances in the kitchen, to dual sinks in the bath, to a large yard or a garage. We’re all feeling the pain at the pump. Unless you decide to walk, bike or take public transportation, you might feel stuck. But all is not lost. Here are some fuel-efficient driving techniques that can help you save hundreds of dollars in fuel each year.

We’re all feeling the pain at the pump. Unless you decide to walk, bike or take public transportation, you might feel stuck. But all is not lost. Here are some fuel-efficient driving techniques that can help you save hundreds of dollars in fuel each year. Today, businesses have to grapple with vast amounts of data from different sources, including emails, mailing lists, customer orders, system logs, mobile apps, social media networks, etc. This data is crucial to businesses in various ways. When analyzed, a business can identify operational issues, personalize the customer experience and manage supply chains – all contributing to better decision-making.

Today, businesses have to grapple with vast amounts of data from different sources, including emails, mailing lists, customer orders, system logs, mobile apps, social media networks, etc. This data is crucial to businesses in various ways. When analyzed, a business can identify operational issues, personalize the customer experience and manage supply chains – all contributing to better decision-making. Supreme Court Police Parity Act of 2022 (S 4160) – In response to potential threats and protests outside the homes of Supreme Court judges following a leak of their preliminary judgement on a case related to Roe vs. Wade, this bill authorizes extra security for the justices and their families. Specifically, Supreme Court justices and their families would be provided with security detail similar to that of other top government officials and families in the executive branch (e.g., the president and vice president) and legislative branch (e.g., Speaker of the House and Senate Majority Leader). This type of detail generally cannot be declined. The bill was introduced by Sen. John Cornyn (R-TX) on May 5. It passed in both the Senate and the House on June 14 and was signed into law by the president on June 16.

Supreme Court Police Parity Act of 2022 (S 4160) – In response to potential threats and protests outside the homes of Supreme Court judges following a leak of their preliminary judgement on a case related to Roe vs. Wade, this bill authorizes extra security for the justices and their families. Specifically, Supreme Court justices and their families would be provided with security detail similar to that of other top government officials and families in the executive branch (e.g., the president and vice president) and legislative branch (e.g., Speaker of the House and Senate Majority Leader). This type of detail generally cannot be declined. The bill was introduced by Sen. John Cornyn (R-TX) on May 5. It passed in both the Senate and the House on June 14 and was signed into law by the president on June 16.